2025

Resilience Pays:

Investing and Financing for Our Future

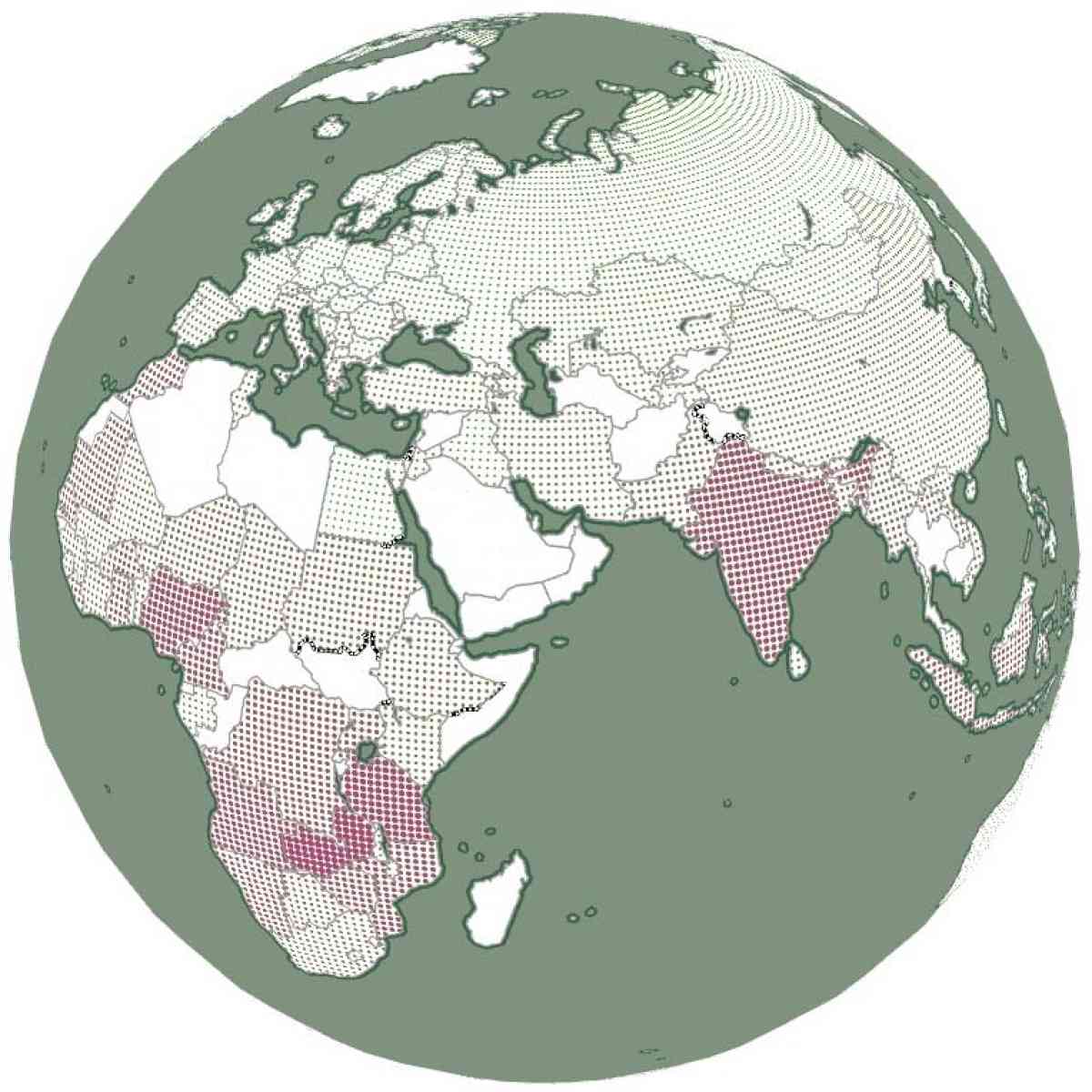

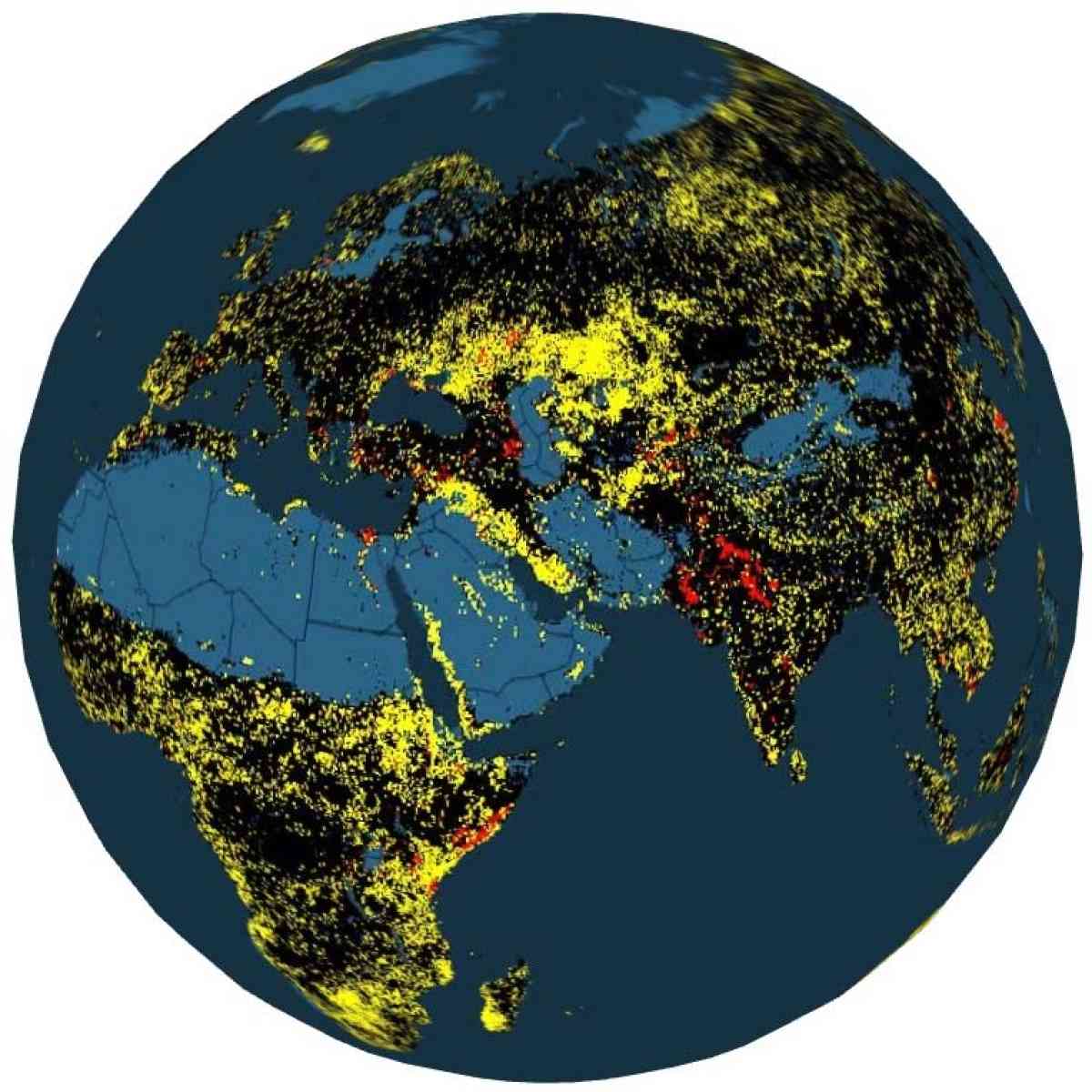

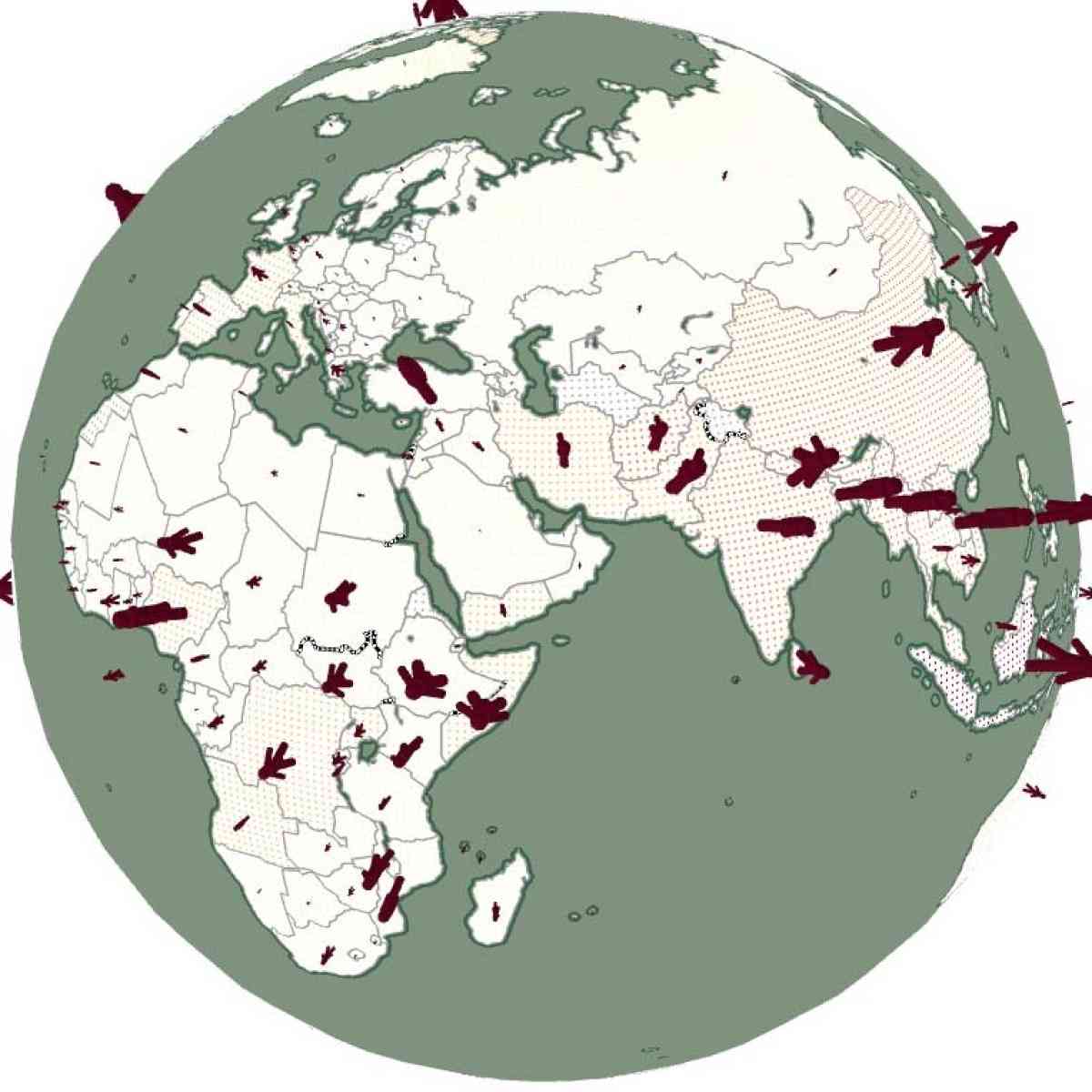

GAR 2025 looks at some of costliest hazards, for example this animation shows the expected impact of hazards on GDP from the year 2030 to 2100. Explore alternative scenarios and more interactive GAR 2025 maps. | Animate globe Pause animation

The global cost of disasters is growing: The economic burden of disasters is intensifying. While the direct costs of disasters averaged $70–80 billion a year between 1970 and 2000, between 2001 and 2020 these annual costs grew significantly to $180–200 billion.

But the real cost is far higher.

Disaster costs now exceed over $2.3 trillion annually when cascading and ecosystem costs are taken into account. The Global Assessment Report (GAR) 2025: Resilience Pays: Financing and Investing for our Future highlights how smarter investment can re-set the destructive cycle of disasters, debt, un-insurability and humanitarian need that threatens a climate-changed world.

Keep reading to learn more about the challenge and the choice ahead or download the PDF report.

Disasters: the world's growing annual bill

Global Disaster Damage Losses (2000-2023)

Total disaster costs are now exceeding $2.3 trillion annually when indirect and ecosystem impacts are included. But, just as the costs of disasters have been under-estimated, so have the benefits of investing now to reduce disaster risk.

This figure is nearly ten times the annual direct losses reported in official figures. And while these numbers are estimates, the risks they represent are real.

For comparison, a national debt of just $300 billion was enough to trigger the European sovereign debt crisis. Disaster risk is increasingly a systemic threat to financial stability on a global scale.

This year’s Global Assessment Report on Disaster Risk Reduction examines the risks posed by disasters from now to 2050 and presents an indisputable case for action. This report clearly shows that investing in disaster risk reduction saves money, saves lives, and lays the foundation for a safe and prosperous future for us all. I urge all leaders to heed that call.

António Guterres

United Nations Secretary-General

As we approach the Fourth Financing for Development Conference later this year, the GAR 2025 carries an important message for us all: investment in disaster risk reduction not only provides a great return on investment, it is essential for our common future.

Kamal Kishore

Special Representative of the United Nations Secretary-General for Disaster Risk Reduction, and Head of the UN Office for Disaster Risk Reduction (UNDRR)

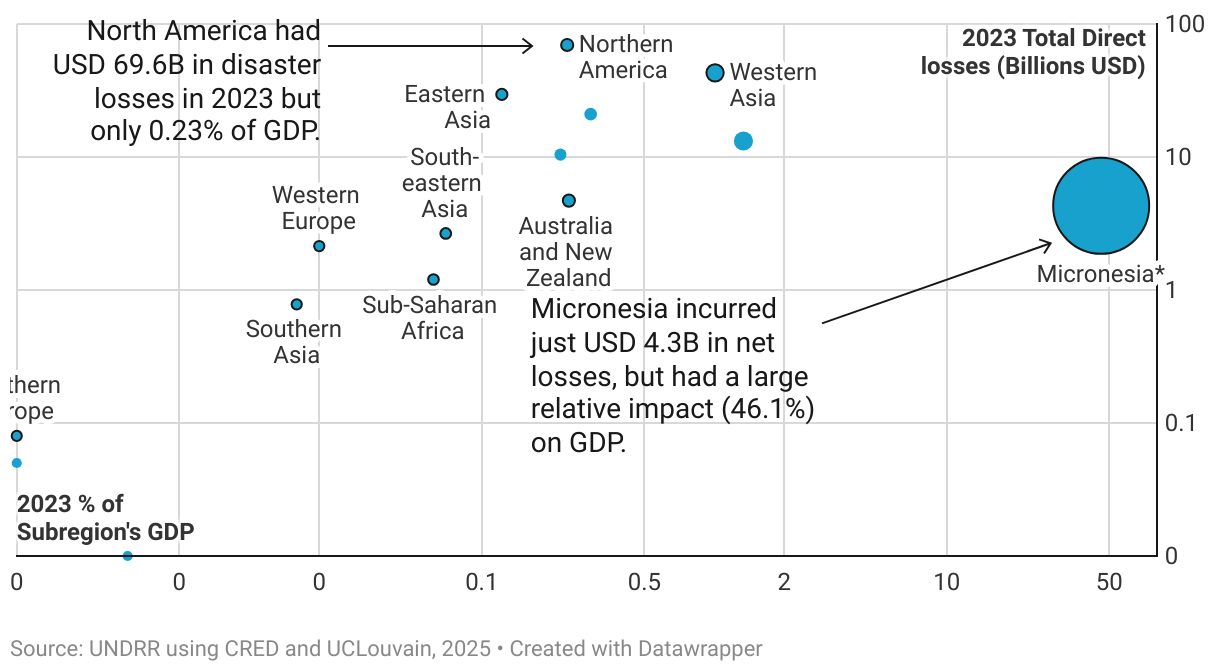

Size matters

In 2023 North America had the greatest economic exposure to disasters, with $69.57 billion in direct losses, however, these represented a relatively modest share (0.23%) of GDP. Micronesia, on the other hand, incurred a fraction of these net losses –just $4.3 billion – but with a far greater relative impact (46.1%) on its subregional GDP.

When losses to health, education, livelihoods, ecosystems and supply chains are factored in, the global bill becomes staggering – closer to $2.3 trillion each year in indirect costs.

When disasters occur, households lose assets and income, shrinking tax revenue. Governments need to borrow more. As debt becomes riskier, interest costs spiral. Soon, there’s no budget left to fund recovery. Smaller, less resilient economies are hit hardest.

Drawing on dozens of positive examples from around the globe, this report shows how effective disaster risk reduction (DRR) investment can accelerate both sustainable development and economic stability at a time when catastrophic risk is increasing globally.

Investing in resilience for economic stability

There is a stark mismatch between the increasing levels of global risk and current investment in resilience.

8) Disasters are already exerting a substantial macroeconomic toll, from weather-related events such as floods, storms, drought and extreme heat to major hazards like earthquakes — and this toll is expected to rise with the growing frequency and severity of these events as the climate changes. Without urgent action to close the gap between risk and investment, the financial and economic consequences will become increasingly difficult to manage.

When disasters occur repeatedly, economic growth often slows and debt increases. Developing countries, particularly small island developing states (SIDS) and least developed countries (LDCS), face the dual challenge of higher exposure to hazard risk and limited access to resources for risk reduction. In such situations, it becomes increasingly expensive to insure or otherwise transfer risk, and more money is spent on humanitarian responses as disasters are not prevented. But this is not inevitable.

To create a more stable investment climate, governments, multilateral institutions, the private sector and households need to rethink and realign their investments to better protect current and future assets. Developing a clear, integrated risk financing approach can help address these challenges and open a pathway toward long-term financial and economic stability.

Acting today can shift the disaster risk narrative—from one of rising costs and instability to one of resilient, inclusive, and sustainable development.

Three Spirals of Unsustainable Development

Disasters don’t just cause damage. They set off three downward spirals that deepen crises and turn disasters into systemic collapses.

Spiral One: Increasing Debt, Decreasing Income

The first negative spiral occurs when a lack of disaster risk reduction leads to recurrent excessive losses, in the process reducing household income and depleting national assets.

Given the interconnectedness of today’s economic systems, even relatively localized disaster-related impacts can have wider repercussions on national and global economies. When households and businesses incur losses in the wake of disasters, many households cut their expenditure while companies are forced to reduce their investments in growth. This, along with the redirection of government funds to provide urgent emergency relief, can cause the overall economy to shrink. Since GDP is essentially the sum of what consumers spend, businesses invest and governments fund, as well as the balance of trade, in many cases these reductions add up to a lower GDP.

Show moreExplore the data interactively

Spiral Two: Unsustainable Risk Transfer

Even in wealthier regions such as the European Union, only about a quarter of climate-related catastrophe losses are currently insured. As a result, central governments are shouldering an increasingly heavy burden of hazard-related risk.

Low insurance penetration also limits the ability to share risk widely, particularly in developing countries where few assets are protected: for instance, insurance coverage remains below 1% in countries like Bangladesh, India, Vietnam, the Philippines, Indonesia, Egypt and Nigeria. Although precise figures are scarce, the gap is clear. In 2018, an estimated $163 billion of assets worldwide were underinsured, leaving an exposure gap that threatens livelihoods and global prosperity.

Show moreExplore the data interactively

Spiral Three: Respond-Repeat

The third negative spiral of disaster risk in financial systems is related to the humanitarian response cycle. Emergency relief in the wake of disasters saves lives, but is often expensive and not designed to have a long-term impact on disaster recovery or to address underlying vulnerabilities.

Reducing risk or even preventing disasters is a far better investment. Studies show that $1 spent on disaster risk reduction delivers an average return of $15 in terms of averted future disaster recovery costs. Currently, most disaster financing focuses on post-event response and recovery rather than preventative disaster risk reduction, with pre-arranged financing accounting for a very small fraction of crisis funding. This approach not only perpetuates vulnerabilities, but also increases long-term costs for recovery and rebuilding.

Show moreExplore the data interactively

A hazardous future is not inevitable

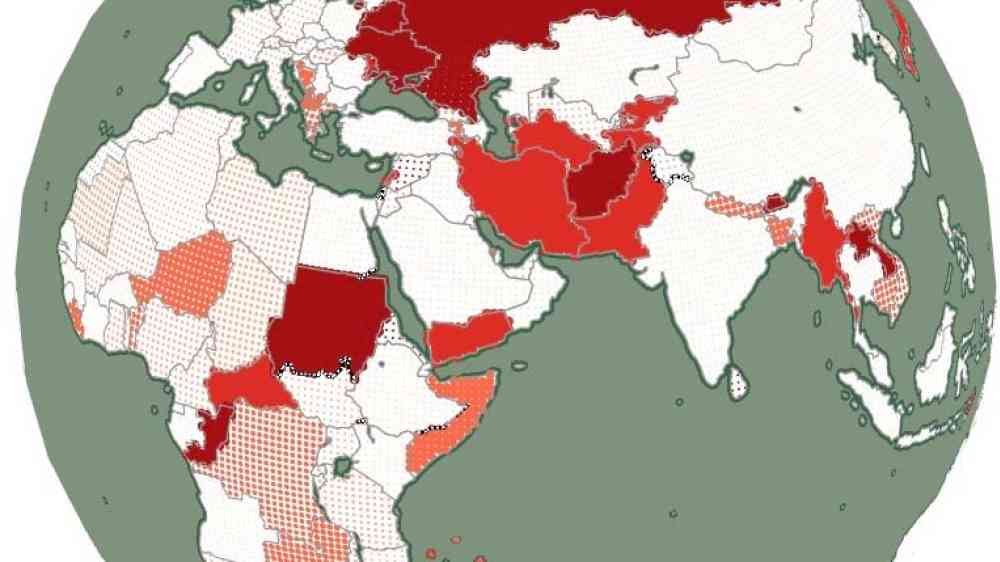

The world is facing an increasingly volatile future. Human choices – from energy consumption to land use planning – play a crucial role in shaping future vulnerability and exposure.

For example, seismic risk is primarily increasing not because the hazard is getting stronger, but because current human action (such as unsafe housing construction in seismic zones) is putting more people and asset in harm’s way.

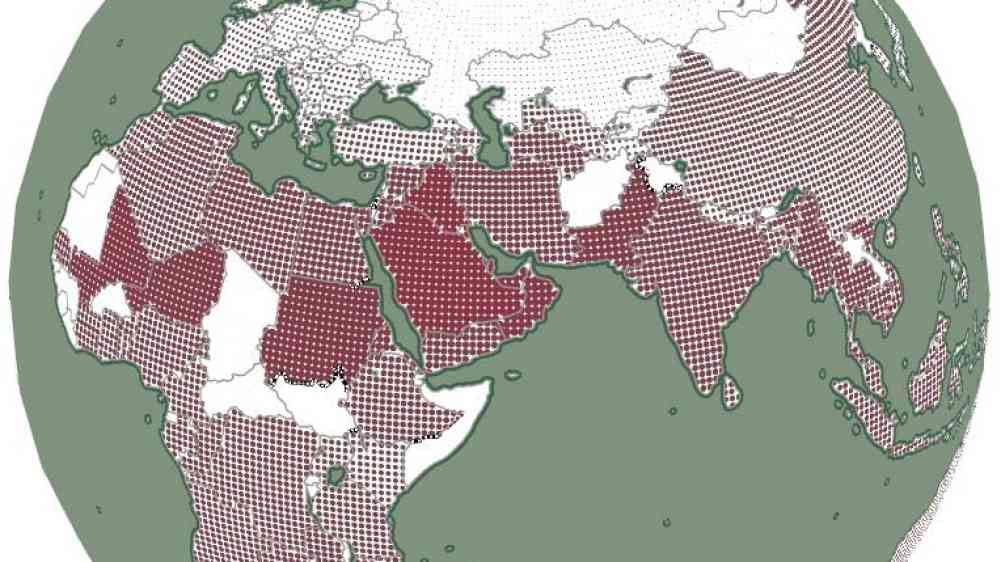

GAR 2025 explores possible future trajectories and economic analysis presenting opportunities to steer toward a more positive path." It particularly highlights the imperative to stop disaster cycles of costly response and slow recovery that hinder long-term economic development and decrease household income growth. It makes clear that unless disaster risk can be reduced, climate-driven disasters may affect future household income growth significantly between now and 2050.

While the model indicates significant regional variations, data suggests a decline in income growth ranging from 11% to 29%. Lower-latitude low-income areas face the most pronounced losses- but all countries would be negatively affected.

Urbanization is currently increasing disaster risk, but that doesn’t have to continue.

Approximately 1.2 billion people are expected to be living in cities by 2050 compared to 2020. This growth will be heavily concentrated in the Global South, accounting for 98% of the total. Ensuring these new buildings are safely situated and adequately constructed could potentially save lives while also safeguarding sustainable development, particularly in rapidly urbanizing locations.

Explore further

Your choice

Two starkly different paths, “Generation Jolt” and “Generation Regeneration”, illustrate potential futures the world could follow between now and 2050, as envisioned by the United Nations Future Lab.

Our choice shapes the next generation

The decisions made today will shape the lives of the next generation in a multitude of ways.

- Generation Jolt exemplifies the extremes of a high-risk, high-regret future, where resilience investment is lacking, and extreme climate and disaster impacts take a toll on people, planet and prosperity.

- Alternatively Generation Regeneration envisions a comprehensive approach to resilience-building, driven by renewed global cooperation, flexibility to adapt, a transformation in value systems and a revolutionized financial sector.

A way forward

Risks can be transformed into opportunities through investments in resilience building.

At present, however, while resilient investments can yield considerable benefits, often repaying their upfront costs many times over, both private sector adaptation and resilience investment and Official Development Aid (ODA) funding remains insufficient, particularly in developing countries.

Given the potential costs of inaction, the stakes could not be higher. A growing body of research makes clear that disaster losses are already considerably larger than mitigation costs. This is particularly true once the potential compounding economic benefits of disaster risk reduction and climate change adaptation are factored in. For example, long-term savings from investment in resilience and coping mechanisms can reach 300% for droughts and 1,200% for storms in sub-Saharan Africa. These large benefits often are associated with programmes like disaster preparedness and public health measures involving low costs but yielding high returns. High benefits are also found in contexts where adaptation involves marginal shifts in production, such as when farmers switch crops, or when improvements in building design help prevent the collapse of infrastructure. Indeed, some sectoral studies report benefit-cost ratios ranging between 100% and 900% for climate adaptation measures.

To succeed, however, adequate investment in resilience is needed at scale. To realize the benefits described above, the necessary resources must first be in place to enable these investments. At present, however, there remains a considerable funding gap in translating disaster resilience policies into concrete actions. This is evident even within the climate change adaptation community: for instance, a recent survey of selected National Adaptation Plans found that around half had failed to adequately cost the financial outlay required for them to be implemented in practice.

This reflects a wider mismatch globally between the levels of adaptation financing needed versus what is available, particularly in low-income countries. Annual financing needs and modelled costs of adaptation for developing countries are both considerably larger than current finance flows. Even if the 2019 Glasgow Climate Pact’s target of doubling the amount of adaptation finance available for developing countries is achieved, this would only address a small portion of the deficit.

Breaking the Spirals

Pragmatic action now to reduce disaster risk in advance can slow and potentially even reverse each of the negative spirals.

Doing so requires a shift in how governments, financial institutions and the private sector approach investments: rather than being an afterthought, resilience must be integrated into project design and development and throughout the asset lifecycle.

Breaking Spiral 1: Protecting household income and ensuring more sustainable debt

GAR 2025 provides dozens of examples where smarter, more risk-infomed investments are reducing or even preventing disaster losses despite the start realities of a volatile risk future:

- Household level

Household level

- Assess risks to homes, assets, pensions.

- Invest in resilience (e.g., strengthen structures, improve drainage, link to early warning systems).

- Advocate for community resilience (e.g., better infrastructure, risk analysis, building codes).

- Purchase insurance or join solidarity groups for recovery support.

- National level

National level

- Integrate DRR into finance planning:

- Understand disaster financial impacts (direct + indirect).

- Analyze DRR finance landscape.

- Identify funding needs and gaps.

- Match with suitable finance tools.

- Develop a comprehensive DRR finance strategy.

- Request local governments to make risk information open and accessible.

- Request regular tracking of the resilience of pension funds and other investments to potential disaster risks.

- Make provisions to learn lessons after disasters and to put in place mechanisms to accelerate the speed of recovery.

- Target initiatives towards populations who may have specific needs in case of disasters such as persons with disabilities.

- Invest in resilient infrastructure (net economic and social benefits).

- Strengthen governance (land use planning, risk analysis in project approvals).

- Use debt-for-resilience swaps to free capital for DRR.

- Integrate resilience into credit ratings to lower borrowing costs.

- Establish standards and taxonomies for identifying resilience investments.

- Implement budget tagging to track and optimize DRR and climate adaptation funding.

- Integrate DRR into finance planning:

- Private sector level

Private sector level

- Assess and mitigate risks in operations and supply chains.

- Use green bonds with resilience components for infrastructure and climate adaptation.

- Apply blended finance models (e.g., Project Gaia) to share investment risks.

- Leverage carbon finance for resilience co-benefits (e.g., mangroves, agroforestry).

- Disclose climate risks to maintain investor confidence and access to capital.

- Consider developing disaster resilient product lines and services.

- Global level

Global level

- Set resilience funding criteria in loan programs and infrastructure projects.

- Introduce flexible repayment terms (e.g., hurricane clauses).

- Offer concessional financing and support debt-for-resilience swaps.

- Promote successful projects to build investor confidence.

- Provide technical assistance for layered DRR financing strategies.

Breaking Spiral 2: Fixing risk-transfer finance

- Household level

Household level

- Purchase insurance or join solidarity groups for recovery support if possible.

- Plan ahead for how you and your family would cope with the most likely hazards in your area, and connect with neighbors and local authorities to make sure you are prepared.

- If available check insurance coverage carefully and have a financial recovery plan.

- Try to have access to an emergency fund that can help speed your recovery if you are impacted by a disaster.

- National level

National level

- Invest in improving risk data and analytics and in national modeling and foresight capacity.

- Require insurance companies to publish coverage and non-renewal data.

- Consider re-insurance coverage/ risk pools to buffer against GDP impacts of major shocks

- Conduct regular budget reviews to track DRR investment, including which assets are covered by risk transfer solutions such as insurance should a disaster occur.

- If your country partners with international financial institutions discuss options for putting in place contingency finance or repayment freezes after disasters.

- Private sector level

Private sector level

- Consider insurance cover to buffer against potential losses in the case of a disaster.

- Look at how to spread the risk across supply chains and business units in case of a disaster to enable faster recovery after shocks.

- Global level

Global level

- Institutionalize repayments freezes after major disasters for loan recipients.

- Innovate to extend risk sharing options to reduce the potential for debt default in the case of disasters.

- Support development of regional or global risk transfer mechanisms, particularly for SIDS and LDCs.

Breaking Spiral 3: Preventing the response-repeat spiral

- Household level

Household level

- Request your local government to make risk information open and accessible, and check what actions are expected in the case of an extreme hazard event.

- Take steps to reduce disaster risk in your home, and assess risk in advance if you move.

- Consider who in your community may have specific needs in case of disasters such as persons with disabilities or elderly family members and discuss with them how to make sure they are well accommodated even in case of a disaster.

- Keep learning about how disaster risk is changing in your area, and opportunities to prevent risk.

- National level

National level

- Scale up anticipatory action and finance.

- Increase the percentage of aid activities targeting disaster risk reduction beyond the current global level of 2%.

- Private sector level

Private sector level

- Ensure you are aware of potential disaster risks to your premises, supply chains and business, and reduce exposure were possible.

- Have a clear business continuity plan for disasters and make sure staff are able to follow it.

- Insure losses where feasible and have a financial plan for accelerating recovery.

- Global level

Global level

- Extend coverage of Anticipatory Finance facilities for vulnerable countries.

- Hard-wire resilience investment into all new green transition projects.

- Develop and apply guidelines on integrating DRR into national lending.

- Require risk reduction to be explicit in humanitarian project design and approval.

Investing and financing for our future

Against this backdrop, investing in disaster risk reduction is no longer optional — it is essential for protecting financial stability and enabling long-term development.

Act now: Resilience pays

Disaster risk is increasing as more frequent and intense hazard events, unsafe urbanization and ineffective development, put more people and assets in harm’s way.

Disasters are having profound macroeconomic impacts, with direct losses estimated at over $200 billion annually or over $2.3 trillion when cascading and ecosystem costs are taken into account.

Current investment patterns fuel spirals that increase debt and decrease income, foster un-insurability and perpetuate an expensive dependence on humanitarian assistance. Disasters are also increasingly associated with credit rating downgrades. Action is essential to protect societies, property values and wider financial and insurance systems.

All countries are suffering. Human impacts are more acute in the global south, but economic losses and un-insurability are growing fastest in more developed countries. The world cannot afford this waste, when so many of these losses are preventable. But just as total disaster costs have been underestimated, so have the benefits of disaster risk reduction in both developed and developing countries. GAR 2025 outlines highlights dozens of examples where smarter, more risk-informed, investments are reducing or even preventing disaster losses despite the stark realities of our volatile climate future. It makes clear that managing risk for the 21st century requires action in six key areas as outlined below.

- 1. Democratize risk understanding

1. Democratize risk understanding

Quality risk information aligned to local realities is fundamental to directing investment effectively to prevent, reduce and manage risk. Risk information needs to be standardized, accessible, comparable, and, as much as possible, open source. But most of all it needs to be global. All countries and markets suffer when risk knowledge is sold only to the highest bidder.

While hazard information is improving globally, governments need to do a better job of connecting this to exposure and vulnerability data to better pinpoint risk. As outlined in Chapter 4, doing so can make pro-poor investments more effective, accelerate disaster recovery and protect infrastructure.

Equally important, both the public and private sectors need access to robust risk information and clear analysis of their likely average annual losses, and, in the case of a larger events, their probable maximum losses. This data must be useable by governments, financial markets, central banks and disaster managers. Metrics need to be tailored to local realities and meet the needs of a wide range of stakeholders, such as central and local governments and project planners. This can enable financial decision makers to begin prioritizing risk reduction actions by geographic area and by key hazards over the medium to long term. Risk metrics should be complemented by resilience indicators, making the benefits of investing in resilience clearer and easier to integrate into decisions. Harnessing both local knowledge and technological advances in machine learning and the appropriate use of artificial intelligence can accelerate trend analysis and the application of new insights into risk.

- 2. Use public financing and regulation to break the risk-creation addiction

2. Use public financing and regulation to break the risk-creation addiction

Physical disaster risks now need to be monitored and managed like any other potential risk to the financial system. What is often seen as unpredictable volatility, or even uncertainty, can in fact be distilled into probabilities and expected losses that can be managed and budgeted for. Governments have a role in setting guardrails, in spreading learning, and in improving access to quality risk data. Metrics and taxonomies exist that can be enhanced to increase their coverage and quality through public-private collaborations and standard setting- as UNDRR has already been doing with key partners.

Governments can lead by ensuring disaster risk financing strategies are fit for the future and a core part of their operations. These strategies need to inter-lock three elements: risk reduction, risk transfer and improved risk management and be based on quality risk information tailored to a countries’ specific exposure, vulnerability and hazard profile.

When implemented effectively, the evidence clearly shows that resilience pays- it saves lives and reduces the scale of humanitarian catastrophes. Even small, relatively low-cost actions, such as accelerating post-disaster recovery support to households, can yield lasting benefits by stabilizing domestic incomes and helping small businesses stay afloat. These actions also buffer against GDP losses from disasters that can balloon levels of debt, decrease credit ratings and derail development. When disaster risk reduction works, emergencies are prevented, and development investment goes further.

Reaping the rewards of resilience also requires ring-fencing disaster risk reduction budgets to empower responsible agencies and mainstreaming disaster risk reduction across sectors and plans. It means putting in place appropriate accountability mechanisms, including budget tagging and tracking systems for DRR-related expenditures. And it means keeping track of how ministries have articulated and allocated funds across the layers of risk management and systematically capturing lessons on what worked and what needs improvement after disasters.

Measuring disaster resilience across sectors is essential to ensure that standards are applied consistently to public investments—both now and in the future. This, in turn, is important for entities such as public pension funds so that younger generations remain confident that the contributions they make today will retain their value in the future.

- 3. Innovate to keep risk transfer and insurance sustainable

3. Innovate to keep risk transfer and insurance sustainable

Risk transfer mechanisms such as insurance can no longer thrive unless governments and companies ensure their actions are more resilient to disaster shocks. To quote Prime Minister Mia Mottely of Barbados, “if it is not insurable it is not investable.” Risk transfer has great potential to incentivize risk reduction: if a country invests in risk reduction, insurance premiums should come down. When insurance companies are required to publish coverage and non-renewal data annually, it sends a powerful signal to markets about the price of unsafe infrastructure, supply chains and areas where risk is increasing. And as volatility in hazard patterns increases, scaling up the pool of people and assets protected by public and/or private sector-backed risk transfer mechanisms is essential to take resilience-building to scale.

Making this work will require insurers to evolve. Cover should no longer be priced based on replacement cost alone. It needs to enable rebuilding to a standard that is fit for the future, and products need to be better adapted to their specific contexts. Insurance products have often struggled when transplanted wholesale from developed to developing countries without adaptation. In many cases, this has created affordability challenges or eroded trust between policyholders and insurers. A more tailored approach—one that supports insurance in easing the relief burden on governments while protecting consumers—is essential if risk transfer tools are to succeed across both developed and developing contexts, as illustrated by the case studies presented in chapters 4 and 6.

Beyond domestic and commercial insurance, finance for adaptation and loss and damage are among the types of risk-sharing instruments that offer considerable potential for expansion. Needs-based social safety nets have long functioned in areas such as public health to cover individuals against rare but predictable diseases. The same kind of social safety nets must now emerge at scale to protect low-income workers from infrequent but high-impact disasters (such as periods of extreme heat, when outdoor work is impossible) and to ensure that recovery assistance reaches poor households quickly.

- 4. Make the business case

4. Make the business case

The private sector accounts for about 75% of capital investment in most economies, but if these investments are not risk-informed, societal resilience will remain out of reach. There is significant scope for innovation and co-financing partnerships to incentivize private sector innovation and investment in disaster risk reduction. Much of the world’s hidden disaster risk is concentrated in companies that are under-insured and increasingly exposed to direct damage, supply chain disruption, and broader financial volatility.

Increasingly investments underpinned by sound plans to manage risk and future volatility will continue attract financing to meet sustainable development targets. Others may struggle. A lack of risk understanding cannot be allowed to hamper investment and development, particularly in the countries that need it most.

Communities and companies alike have centuries of experience in coping with disasters and taking action to reduce risk. Today, at the dawn of a new information age, their capacities can be vastly strengthened by applying artificial intelligence to accelerate learning and analyze trends across many areas of disaster management. At the same time, advances in engineering and emerging resilient technologies offer new opportunities to build more safely and affordably. Industries such as insurance recognize that their expertise in risk analytics has value beyond underwriting— helping to identify and scale up safer, and therefore more investable, infrastructure. These efforts deserve recognition, and ideally incentives, alongside other strategic tools needed to ensure a just and green transition.

- 5. Anticipate shocks to reduce humanitarian needs

5. Anticipate shocks to reduce humanitarian needs

Because resilience-building to date has been insufficient, many vulnerable countries often remain trapped in a vicious cycle of disaster, response and recovery, only to repeat the pattern again and again. The international community has a shared responsibility and interest in breaking the cycle. This requires scaling up anticipatory action and finance, while also increasing the percentage of aid activities targeting disaster risk reduction beyond the current global level of 2%.

It also requires a shift in mindset—recognizing that disasters arise not just from hazards, but from underlying vulnerabilities or heightened exposure that enable hazards to escalate into a humanitarian crisis. Employing low-cost tools, such as disaster forensic analysis, to pinpoint these factors is essential. This is because recovery efforts targeted at reducing core vulnerabilities or the most damaging exposures, are more cost effective and have the greatest potential to prevent future crises.

Reducing humanitarian needs reduces suffering and loss of life. It is cost effective, and it benefits individuals, societies, economies and the environment, even decades after a shock has passed. But reducing needs in the middle of a disaster is impossible: it requires careful proactive risk reduction to prevent hazards from escalating into disasters.

- 6. Leverage the multiplier effect of international financial mechanisms

6. Leverage the multiplier effect of international financial mechanisms

International finance institutions and public planners must harness the power of increasingly globalized financial markets to share risk more broadly, find better ways to prevent fiscal gaps, and support faster, better-targeted recovery—ensuring that disasters do not create humanitarian needs and long-term suffering.

Increasing resilience can deliver significant efficiency gains—and these must be central to how multilateral donors and development banks protect their portfolios from the cascading impacts of disaster volatility. Even relatively modest interventions, such as extending reinsurance-style coverage to absorb a share of GDP losses when LDCs and SIDS are impacted by a major disaster can prevent debt defaults and avert decades of stalled development. Resilience pays, and concrete measures to buffer against disaster shocks should become standard in the design of sovereign loan programs and in the prioritization of official development assistance (ODA).

As multi-lateral systems evolve to address complex challenges such as adaptation and loss-and-damage finance, it will be essential to draw lessons from risk pooling and reinsurance. This requires innovation and sustained learning, but the potential benefits are substantial. There are mechanisms in place that can be strengthened to facilitate this, such as the Santiago Network, which aims to provide much-needed technical assistance to developing countries for building resilience to loss and damage.

In many contexts, tools like ODA, and, increasingly, climate adaptation finance, should be used to help fiscally constrained countries enhance their resilience. This not only supports long-term stability, but also increases the effectiveness of aid, given that disaster risk reduction measures often deliver some of the highest benefit-cost ratios, ranging from 2:1 to 10:1 or more.

Breaking the current destructive cycle of disaster, recovery, and debt is urgent and essential for continued prosperity in a climate-changed world.

The rising costs and intensifying frequency of disasters can no longer be treated as isolated events—they are systemic threats that demand a fundamental shift in how risk is understood, financed and managed globally. By embedding disaster risk reduction at the heart of financial decisions and policy frameworks, governments, businesses and communities can interrupt harmful cycles of vulnerability, loss and debt while accelerating sustainable, equitable development.

The pathway beyond 2030 need not be defined by shocks and piecemeal, unplanned recovery; instead, proactive investment in resilience can pave the way to a future defined by stability, prosperity and sustainable progress. The opportunities for transformative action are clear—now it is up to decision-makers across the globe to seize them.

Resilience is not a cost, it's a catalyst for growth

Download the GAR 2025 full report

Summary for Policymakers:

Explore the evidence for yourself

Earthquakes account for over a quarter (25.6%) of global economic disaster losses.

Recent data suggests that floods account for up to 35–40% of weather-related disaster occurrences.

In some regions, storms account for up to 35% of total recorded disaster costs, driven by high winds, storm surges, and heavy rainfall.

Droughts often unfold slowly, but with far-reaching impacts on agriculture, water supplies, and economic stability.

The direct and indirect economic impacts of extreme heat events already cost tens of billions of dollars each year.

Learn more about the role of disaster risk reduction